10xTravel is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

Neill Drake was living in a van in South America five years ago, guiding Antarctica expeditions and barely making any money. Today, he’s the founder of Antarctica Travel Group (transitioning to Let’s Go Polar), leading a team of eight and processing up to $2 million in credit card spending during peak season.

His business didn’t start as a business at all—it started as a Facebook group to keep track of friends from expedition trips. But that community-driven approach, combined with strategic credit card use as the company scaled, has created both a thriving business and enough points to make travel nearly free.

The Accidental Business: From Facebook Group to Full Agency

Drake’s origin story is unconventional. After leaving the military, he was backpacking across South America, doing work-aways and staying in hostels for free room and board. He guided Antarctica expeditions seasonally, and passengers kept sending him Facebook friend requests after trips.

“After a while, my Facebook didn’t become my Facebook anymore,” Drake said. “I couldn’t keep track of my friends.”

So he created a Facebook group—Antarctica Travel Group—just to consolidate connections with past passengers. People who hadn’t been to Antarctica started joining, asking questions and seeking advice. “Talk to Neil. He knows. He’s the guy,” became the common refrain.

The turning point came when Drake discovered that one of the expedition companies he guided for offered referral fees in their employee handbook.

“I was a backpacker living in a van in South America,” he said. “I wasn’t making any money. That was some money I could start earning.”

The group grew from 2,500 to 5,000 to now about 50,000 members. As an expedition guide who’s been to Antarctica more than 100 times, Drake had experience that traditional travel agents couldn’t match.

“I’ll literally screenshot from my phone,” Drake said. “People ask, ‘Are there still penguins in late February?’ I’ll go through my Google photos, find Feb. 21, 2021, screenshot and send it to them. That is from my cell phone on that day. Anybody who tells you otherwise is lying because I have the experience.”

That authoritative voice turned a Facebook group into a full-fledged travel agency with eight employees.

The Business Model Shift That Changed Everything

For the first few years, Drake’s business model was simple: Clients would book through him, pay the tour operator directly, and, at the end of the season, the operator would pay him commission.

Then about three years ago, everything changed.

“We made some negotiations where a customer would pay us, and then we pay the tour company,” Drake said. “We settle up with them at the end of the year. And they take credit cards, and they don’t charge us a credit card fee.”

This shift meant Antarctica Travel Group was now the merchant of record, processing all customer payments through their own credit cards before paying tour operators. Since the operators accept cards without fees and everything registers as travel spend, it unlocked massive points earning potential.

The Numbers: Seasonal Scale Creates Serious Points

- Off-season (April, May, June): Monthly spend: $10,000 to $30,000

- Peak season (November through March): Monthly spend: $200,000 to $500,000

- Annual credit card spend with one operator alone: $1.5 million to $2 million

- Monthly points earned during peak season: Varies by card, but substantial, given the volume

The seasonal nature of his spending means Drake needs to think strategically about which cards to use when. During the booking season when clients are making final payments 90 days before trips, the spending concentrates heavily over a few months.

The Card Strategy: Category Caps and Status Chasing

Drake’s approach is less about maximum optimization and more about strategic allocation.

Step 1: Max out category bonuses

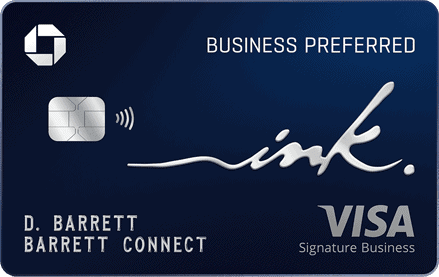

“We have the Chase Ink Business Preferred® Credit Card where we can rack up 3X on travel up to $150,000 spend,” Drake said. “So I hit that $150,000 spend, and then I go to the next card because that one doesn’t do me any favors anymore.”

Step 2: Chase airline status

“I get my American Airlines status by spending on those co-branded cards, and then I move on to the next card.”

Step 3: Capitalize on sign-up bonuses

“A sign-up bonus comes along, and I go on the best card list and see if this is a good one for my journey.”

Drake said he’s not obsessing over whether to use different cards at the gas station. With business spending this high, micro-optimization doesn’t move the needle.

Chase Ink Business Preferred® Credit Card

100,000

bonus points

after you spend $8,000 on purchases in the first 3 months from account opening.

Annual Fee: $95

The Status Play: Executive Platinum in Three Weeks

Drake flies primarily American Airlines between the United States and South America, where his company has operations. With the volume of travel expenses flowing through his cards, status isn’t difficult.

“[My wife and I] are Executive Platinum,” Drake said. “That takes me about three weeks to get my annual Executive Platinum spend, which is about $200,000 put on a co-branded American Airlines card.”

The British Airways Arbitrage Discovery

One of Drake’s biggest aha moments came from understanding earning rate arbitrage, not just redemption arbitrage.

American Airlines is his primary carrier, but earning American miles directly is difficult—mostly 1X miles per dollar spent, except on American Airlines flights, which he books with points.

The solution: Earn British Airways Avios with a credit card that earns 3X points on travel, such as the Chase Ink Business Preferred, then book American flights using Avios.

“An 18,000-point flight with American might be 36,000 points with Avios,” Drake said. But because of the elevated earning rate in the travel category, he can earn more points quicker and then transfer them to Avios. “So it’s costing me more points, but I’m earning those points at a faster rate with the same amount of spend.”

The math works: Earning 36,000 Avios at 3X requires $12,000 spend. Earning 18,000 American miles at 1X requires $18,000 spend. He’s getting the same flight for less total business spend.

“It’s cheaper for me to use more points to get the same flight,” Drake explained. “Add in a 30% transfer bonus to Avios, and now it’s even cheaper for me.”

The Points vs. Cash Back Decision

Drake made an interesting calculation when considering whether to pursue points over cash back.

“If I make a $10,000 Antarctica sale and get that extra 3% cash back, I’m getting $300 extra dollars in commission,” he said. “But I’m getting 10,000 points if I put it on my card. I can do a lot more damage with 10,000 points than I can with $300.”

His example: A $495 flight to Green Bay, Wisconsin, cost him just 9,000 points.

Business Spend vs. Personal Redemptions: The Tax Write-Off Math

As a travel company owner with his wife as a W-2 employee, Drake has flexibility in how he uses points versus cash for business travel.

“If there’s a $1,200 flight and it’s like 80,000 points, I’ll take the business spend for that because it’s a tax write-off,” he said. “You’re not getting a dollar-for-dollar tax break—you’re getting 25% to 35%, whatever your tax bracket is.”

But he doesn’t take this to an extreme.

“Just because I need tax write-offs doesn’t mean we spend $400 on a flight that I can get for 9,000 points. You have to be penny-wise, pound-foolish.”

Drake’s philosophy: Use points strategically for last-minute bookings and personal travel. Use business cash for planned business travel that delivers tax benefits.

The Balance Point: When Optimization Becomes Overhead

Drake is transparent about where he draws the line on points optimization.

“You’ve got so many points and you’re wasting hours of research over 10,000 points,” Drake said. “Just book what makes the most sense.”

The Mistake: Getting Too Greedy with Transfer Bonuses

Drake noted that one mistake he learned was to not get overzealous with transfer bonuses because it could mean you end up with “points parked in places where you’re not going to use them as much.”

Drake transferred heavily to British Airways at one point and ended up with more Avios than he could efficiently use. While the transfer made sense mathematically, the practical reality of booking availability meant those points weren’t as useful as flexible currencies.

The lesson: Transfer bonuses are attractive, but availability and your actual travel patterns matter more than raw point values.

QuickBooks and the Accountant Tax

One challenge Drake wishes he’d known earlier.

“Bookkeepers and accountants are very expensive,” he said.

Every time he opened a new card, he had to add it to QuickBooks, sync everything and manage the integration. At scale, this administrative overhead adds up.

The Philosophy: Match Strategy to Business Stage

Drake’s advice shifts based on where you are in your business journey.

- Early stage (living in a van, low income): Every point matters. Optimize aggressively. He was doing exactly that when he started.

- Growth stage (established business, scaling team): Focus on high-value moves, not micro-optimization. Use strategic card selection based on spend categories and status goals.

- Mature stage (substantial revenue, time constraints): Accept that simplicity has value. Don’t spend hours researching the perfect redemption to save 10,000 points when those hours cost more than the points are worth.

“As entrepreneurs, we’re busy,” Drake said. “Our teams are busy. It’s great to earn points and take awesome trips. But if you or your team are spending too much time managing points and miles, what’s the opportunity cost to the business?”

How He Uses Points: Business and Personal

For personal travel:

- Premium-cabin flights to Europe, South America, Asia

- Last-minute domestic bookings

- Flexible hotel bookings when traveling off the beaten path

For business:

- Employee rewards (sent his COO Ricardo Nisiide to a Chiefs game in Kansas City, Missouri, using points)

- Team bonuses and gifts at Christmas

- Occasional business travel when the redemption is significantly better than cash

For hotels:

Drake actually doesn’t use points much for hotels. His strategy is to show up in destinations and book last-minute for huge discounts.

“We booked a room in Mykonos—private pool out back, $1,200 a night retail,” he said. “We showed up the night before, got three nights there and paid $275 a night for just last-minute bookings.”

He’s Genius Level 3 on Booking.com and leverages Amex Fine Hotels & Resorts when applicable for the benefits and category bonuses.

The Point Balance Philosophy

Drake’s balance swings dramatically by season:

- Low point: About 500,000 points

- Peak (end of Antarctica season): About 2 million to 2.5 million points

He said he has spread across multiple programs but doesn’t stress about it.

His approach: Know roughly how many points you’ll earn annually. Once you’re comfortable you can cover the next year’s travel, don’t hoard indefinitely.

“If you’re in September and you want to go on a trip and you still got 600,000 points left over, maybe this isn’t the best redemption in the entire world, but you know the new year is gonna be coming,” he said. “You’re gonna be making new points. Just spend the points.”

The 4% Crypto Card Consideration

Drake mentioned exploring a cryptocurrency card offering up to 4% back in Bitcoin, noting, “If you believe in crypto and that it’s gonna continue to grow, that’s the next one I’m considering.”

For business owners who’ve maxed out their points earning capacity and believe in alternative investments, converting business spending to appreciating assets rather than travel points represents another evolution in thinking about rewards.

The Bottom Line for Travel Business Owners

Drake went from a military veteran living in a van and barely making money to running an eight-person travel company processing $1.5 million to $2 million annually through credit cards.

His approach isn’t about perfect optimization—it’s about strategic allocation that matches his business reality:

- Maximize category bonuses until they cap out

- Chase status on airlines he actually flies

- Capture sign-up bonuses when the timing aligns with big spending periods

- Don’t sweat the small optimizations that consume mental bandwidth

- Use points primarily for personal travel and occasional business perks

- Accept that redeeming is harder than earning, and sometimes paying cash is fine

For business owners in travel, consulting or any industry with high monthly spend, you don’t need to optimize every purchase to generate substantial points value.

Drake’s business model of being the merchant of record for customer payments before paying suppliers is particularly powerful. If your business involves collecting payment upfront and then paying vendors or contractors, and those vendors accept credit cards without fees, you’re sitting on a massive points opportunity.

At $200,000 to $500,000 monthly spending during peak season, points accumulate faster than most business owners expect, even at base earning rates. That was Drake’s biggest surprise about business expenditure, he said.

The key is getting started, choosing decent cards and not overthinking it. The points will come. Then you can decide whether to fund Antarctic expeditions, gift travel to employees or just make your personal travel nearly free.

Related: How a Custom Home Builder Funded 30 Years of Family Travel

New to the world of points and miles? The Chase Sapphire Preferred® Card is the best card to start with.

With a bonus of 75,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening. , 5x points on travel booked through the Chase TravelSM Portal and 3x points on restaurants, streaming services, and online groceries (excluding Target, Walmart, and wholesale clubs), this card truly cannot be beat for getting started!

after you spend $8,000 on purchases in the first 3 months from account opening.

Annual Fee: $95

Editors Note: Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

10xTravel is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

Editors Note: Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

bonus cash back

after you spend $6,000 on purchases in the first 3 months from account opening

to use on Capital One Travel

in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

bonus points

after you spend $5,000 on purchases in the first 3 months from account opening.

Membership Rewards® Points

after you spend $6,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.