10xTravel is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

Note: Some of the offers mentioned below may have changed or may no longer be available. The content on this page is accurate as of the posting date; however, some of our partner offers may have expired. You can view current offers here.

If you’ve resolved to pay closer attention to your financial health, you have probably read at least a dozen articles that explain how your credit score works. It’s a topic that makes for an attention-grabbing headline, so naturally, the financial news outlets and blogs love to churn out a credit score article every few weeks.

I typically read these articles to see if they have anything new to say.

Spoiler alert: They don’t.

In fact, I have found that they all have two things in common:

- They contain way too much technical information, and

- They are mind-numbingly boring

No wonder most of us have a hard time understanding how credit scores work.

With that in mind, I am going to try to make this topic easier to understand. First, I am going to walk you through how credit scores are calculated. Then, I’ll summarize with 4 basic rules that will help you build and maintain a solid credit score and keep it going forward.

Let’s get started!

Your Credit Score

Since the day you turned 18, many of your major financial decisions have been monitored by three credit bureaus (Equifax, Experian, and TransUnion) and compiled to produce a three-digit score that reflects your ability to manage money. That score, commonly called your “credit score” (or FICO score), ranges from 300-850 and it is used by creditors to determine how likely you are to repay any debt that you have.

The higher your score, the more likely you are to repay your debt, and therefore, the more likely you are to qualify for any sort of credit card or loan.

High scores = good. Low scores = bad. Pretty simple so far.

Now let’s take a look at how your credit score is calculated.

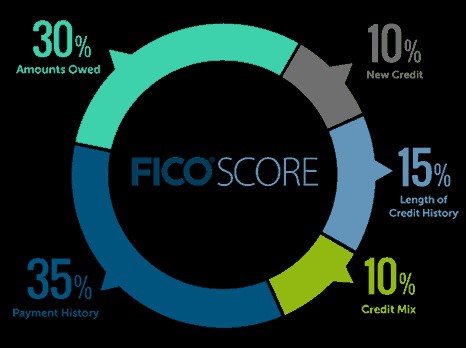

Your credit score is calculated by taking dozens of data points and grouping them into five major categories. Let’s take a look at each one individually.

Payment History (35%)

Payment history is the single most important factor that goes into determining your credit score. Naturally, lenders want to know how often you have paid past credit accounts on time.

Not only is your payment history the most heavily weighted metric, but it is also the most volatile. Missing just one payment could cause your score to drop by over 100 points (Ouch!), which could easily prevent you from qualifying for any sort of credit card or loan.

The solution here is simple. These days, it’s common practice to have the ability to set up automatic payments through your creditor. Set it and forget it, and keep that 35% as high as possible.

Amounts Owed (30%)

The second biggest factor in determining your credit score is the amount of debt you owe. This metric is broken down into a few subcategories.

- Total Amount Owed: This is the total amount of debt that you owe on all of your credit cards, loans, etc. Generally speaking, the less debt that you have, the better your score will be.

- Total Amount Owed by Account: This is a measure of how much debt you have on each of your accounts, proportionally. This is commonly referred to as your credit card utilization, which is expressed as a percentage of your credit limit.

For example, if you have a $1,000 limit on a credit card and have a balance of $500, then your utilization for that card would be ($500/$1000=) 50%.

The lower your utilization, the higher your credit score will be. However, holding a 30% utilization is still considered to be a healthy balance. This shows that you can keep yourself away from a long cycle of minimum payments, but also demonstrates that you’re still actively building your credit history. If you can’t pay your balance in full each month, try to keep your utilization below 30%.

- How Many Accounts Have Balances: Carrying a high balance on a large number of your credit lines indicates that you may be a high-risk borrower and can lower your credit score.

- Amount of Installment Loans Still Owed: Paying down installment loans (mortgages, car payments, etc.) is a good sign that you are able to manage and repay debt. Like credit card payments, you always want to make your installment debt payments on time and in full.

Length of Credit History (15%)

Length of credit history is a measure of the amount of time that you have had your credit accounts. This metric takes into account the age of your oldest account, the age of your newest account, and the average age of all of your accounts. In general, a longer credit history will lead to a higher credit score. This is because you’ve had time to establish your credit and build trust with creditors, making you a candidate for new credit lines in the future.

Additionally, you may be tempted to close older accounts that you’ve paid in full but those are important for your credit history. It’s best to keep those accounts open as they more accurately demonstrate the length of your credit history and they can help prove that you’re a trustworthy borrower, thus boosting your credit score.

New Credit (10%)

New credit is a measure of how many credit accounts you have opened recently. By opening a lot of new accounts in a short period of time, you are hinting that you might have fallen into recent financial disarray, flagging you as a potentially risky borrower. This will likely cause your credit score to fall. Try to avoid this whenever possible.

Types of Credit Used (10%)

This factor looks at your mix of credit cards, retail accounts, installment loans, and mortgage loans. You ideally want to have a healthy balance of credit card debt and installment loans to show that you know how to manage both types of debt. If possible, it’s a good idea to diversify the types of credit you maintain.

As you can see, even this condensed version, managing credit can be a bit tricky. Now let’s boil it down to the bottom line.

- Make sure you understand how your credit score works. By reading this article, you’ve already taken that first step. Congrats!

- Always make your payments on time. No amount of credit score strategy will ever be able to make up for the damage that late or missed payments will do to your credit score. To avoid this, set up AutoPay whenever possible.

- Build a solid credit history. The more credit history you have, the more evidence there is that you are a responsible borrower.

- Keep your credit card balances low. If you can’t pay your balance each month, try to keep your utilization below 30%.

And since most people who are new to points and miles are initially worried about hurting their credit score, it’s possible to see here that there are just a few safeguards you have to keep in mind to avoid hurting your credit score. The biggest two are to make sure you pay your credit card on time and to keep you overall (and individual card) utilization below 30%. Getting new cards, and even getting denied for new cards, will not have a significant impact on your credit score.

By understanding how your score works, always making your payments on time, building a solid credit history, and keeping your balances low, you will easily maintain a good credit score.

Final Thoughts on Credit Scores

At 10xTravel, we’re passionate about helping you leverage your credit into incredible travel experiences, like using your points and miles to explore exciting destinations such as Israel or Germany. Once you understand how to manage your credit, you’ll be able to stockpile points and miles in no time!

New to the world of points and miles? The Chase Sapphire Preferred® Card is the best card to start with.

With a bonus of Earn 75,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening. , 5x points on travel booked through the Chase TravelSM Portal and 3x points on restaurants, streaming services, and online groceries (excluding Target, Walmart, and wholesale clubs), this card truly cannot be beat for getting started!

Editors Note: Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

10xTravel is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

Editors Note: Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

bonus cash back

after you spend $8,000 on purchases in the first 4 months from account opening

miles

once you spend $4,000 on purchases within 3 months from account opening, equal to $750 in travel

bonus points

after you spend $5,000 on purchases in the first 3 months from account opening.

Membership Rewards® Points

after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.