10xTravel is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

The information related to Citi Double Cash Card® has been collected by 10xTravel and has not been reviewed or provided by the issuer or provider of this product or service.

Whether your dog swallows your car keys or you break your tooth on an innocent piece of popcorn, the same thing suffers each time—your bank balance.

Unexpected expenses are an inevitable part of life, but making the most out of them is optional. By seeing these unfortunate situations as opportunities to put a significant amount of spending on a new credit card, you can take the sting out of the bill and earn yourself a points-funded vacation with your next hospital visit or roadside breakdown.

Here’s a definitive guide on how to turn unexpected expenses into more trips, with some tips and workarounds for merchants who don’t typically accept credit card payments.

Using a Credit Card for Emergencies: Things to Consider

Using a credit card to cover emergency spending can offer significant advantages. However, there are some pitfalls to watch out for.

First off, you should treat your credit card like a debit card. Paying your statement balance off in full should be non-negotiable to help you avoid running into double-digit interest rates. Used incorrectly, credit cards can land you in thousands of dollars worth of debt.

If you have an emergency fund, you can still use a credit card to cover the initial expense, allowing you to earn points on your expenditure. You can then use your emergency fund to pay your balance off in full before its due date. This way, you’ll earn points and avoid paying a dime in interest charges.

If you don’t have enough in an emergency fund or savings to cover the cost of an unforeseen emergency in full, you’ll want to focus less on earning points and more on finding the best type of debt product for your situation. If your insurer won’t pay out, you’re unable to borrow money from family members or if your HSA/FSA fund can’t cover you, you’ll want to look for a 0% introductory APR credit card.

A 0% introductory APR credit card allows you to charge an expense to it and pay it back over 12 to 24 months (depending on the issuer), without any interest accumulating. You’ll want to ensure that you have a plan in place to pay the balance off in full by the end of the introductory period, otherwise you’ll run into sky-high interest rates. Ensure you make regular payments to avoid running into a spiral of debt.

Lastly, depending on how big the expense is, you may well end up maxing out your credit limit—either on a single card or even across all your cards. While this isn’t necessarily a problem, doing so will increase your credit utilization ratio far above the recommendation of 30% or less. If you’re planning on applying for other credit cards or debt products, such as a mortgage, you should focus on reducing your credit utilization ratio first, as it affects your credit score.

What if the Merchant Doesn’t Take Credit Cards?

Not all merchants accept credit cards. And even if they do, some may charge a fee to accept them.

Here you have a few options to consider.

The most extreme case is merchants who don’t accept credit card payments. In this case, you can turn to Plastiq to help you pay with a card. Plastiq enables you to pay merchants who don’t accept credit cards by converting your payment into an acceptable format, such as a check or ACH. In return, Plastiq charges a 2.9% convenience fee.

Plastiq can be well worth it, as long as you can get a greater return value than what you pay in fees. For instance, if you charged $4,000 to your card with a convenience fee of 2.9% to earn 80,000 points, you’d pay $116 worth of fees. However, if you can redeem your 80,000 points for 1 cent apiece, you’d still get at least $684 worth of net value out of your points, making it worthwhile.

Alternatively, in some cases, you may be able to avoid having to use Plastiq altogether.

For example, when it comes to car or home repairs, you might be able to order the parts required directly from the supplier and pay them using your card, and then pay the mechanic or contractor using cash (assuming they don’t accept card payments). If the cost of the new parts—be it a new transmission for your car or boiler for your home—is enough to enable you to meet the minimum spending requirement on your card, then you won’t need to use a service like Plastiq to pay the contractor.

In instances where merchants charge a fee to accept credit card payment, compare it to Plastiq and see which one is cheaper.

Whenever you’re being charged a fee to use a credit card, you’re best off paying the amount required to meet the welcome offer only and covering the rest of the bill with cash or a debit card. This way, you’ll minimize fees while maximizing the value of your welcome offer. This can be easier to do if you request an itemized bill, allowing you to pay for each service separately.

Dental Disasters: Smile and Earn Miles

When you hear that ominous crunch as you’re chewing your breakfast, you can expect some hefty bills.

Most dental work typically isn’t included under your standard health insurance plan. And most separate dental insurance policies provide a maximum annual coverage limit of $1,000 to $2,000 and will cover only up to 50% of the bill in instances where major procedures are required.

Luckily, most dentists offer the ability to pay with a credit card. Considering that dental work can easily cost you thousands of dollars, it’s the perfect way to earn a new card’s welcome offer.

Emergency Room Visits: Dream of R&R in the ER

After the drama of surgery subsides and the painkillers wear off comes the real horror—the bill.

Even with the help of health insurance, deductibles can be sky high. Emergency room procedures can easily cost you anywhere from five to six figures. While your insurer may be billed directly for your visit, you’ll still need to pay any deductibles, copayments or coinsurance payments.

Luckily, most hospitals accept credit card payments, allowing you to turn your kidney stones, hip replacement or C-section into a points-funded vacation. Even if you set up a zero-interest payment plan, you can often pay it off using a credit card, saving you from having to pay upfront while earning you rewards in the process.

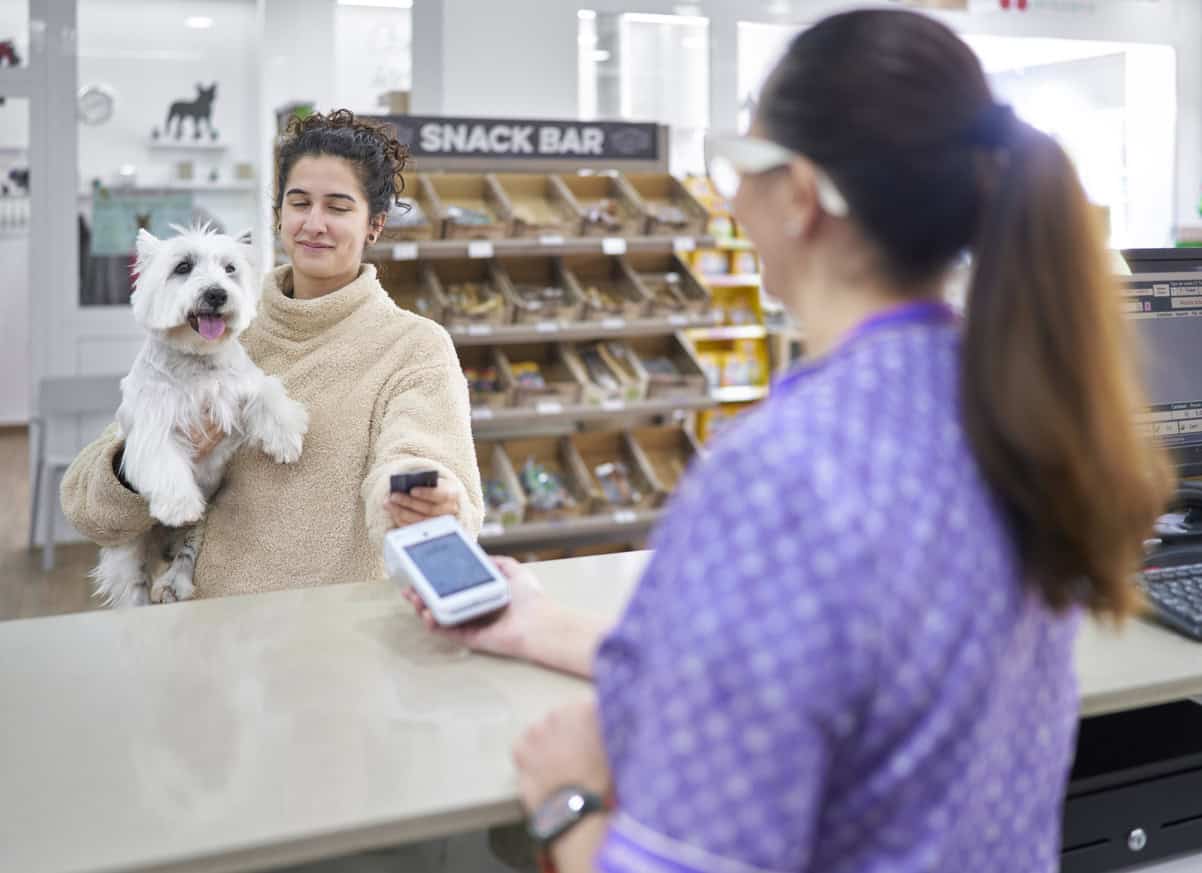

Vet Bills: Turn Your Furry Friend’s Woes Into Free Flights

Young female client picks up her puppy at the vet and pays wirelessly with her credit card

When you realize that your daughter’s favorite Barbie is missing and your dog seems to be choking, it doesn’t take much to put two and two together.

After a frantic rush to the vet’s office and a lengthy and stressful night of waiting, the icing on the cake is the hefty bill you’ll need to pay at the end. While emergency vet procedures tend to cost anywhere between $78 and $1,439, surgery and speciality treatments can easily approach $10,000 or more.

If you have a separate pet insurance policy, you may be eligible for coverage. However, you’ll still need to pay the bill upfront and then file a claim for reimbursement with your insurer.

Thankfully, most veterinary clinics allow you to turn your furry friend’s nightmare into tens of thousands of points by paying with a credit card.

Home Maintenance Repairs: Fix the Leak, Fund a Flight

Home ownership is an expensive project. As durable as our homes may be, things break every now and then. As of 2024, the average single-family household pays $10,433 per year in annual home maintenance costs, according to Forbes.

While homeowner insurance provides fairly extensive coverage, deductibles run high. Likewise, not every event is covered by your insurance policy. General wear and tear, maintenance, sewage blockages, flooding and more isn’t typically covered by your provider.

Turning home repairs into points isn’t always easy, but it can be done.

While large contractors, such as franchised businesses, usually accept credit card payments, smaller independent contractors often prefer cash.

You can work around this by asking to order and pay for the parts required directly using your credit card. You can then pay for the contractor’s labor using Plastiq or pay them using cash if the parts alone already enabled you to reach your card’s minimum spend.

Car Repairs: Let Your Broken Transmission Take You Abroad

Just like homes, cars are an expensive commodity. Whether you’ve been ignoring that pesky check-engine light for months or you have a sudden breakdown, your mechanic’s fees are sure to put a dent in your bank account.

Car repairs cost Americans an average of $1,425 per year, according to the American Automobile Association (AAA). However, if you have major repairs, you could easily be looking at a bill of more than $10,000.

While you might be reimbursed by your auto insurance policy, you’ll still need to pay the cost of the damage and repairs upfront.

Luckily, most mechanics accept credit card payments, making it easy for you to earn points on that broken transmission or new timing belt. And for the few who don’t accept credit card payments, consider paying for the parts yourself using your card and paying for labor costs in cash.

Check out the best credit cards for car expenses and repairs to see how to best maximize the return on your spending.

Legal Trouble: Earn a Return on Your Attorney

At some point in life, you’ll likely need to turn to an attorney for help.

The average retainer fee for lawyers in 2023 ranged between $1,973 and $4,015 according to LawPay, depending on the area of practice and specific case.

Considering that only 8% of Americans have legal insurance, it’s likely that your attorney’s fees will move you into deep out-of-pocket territory.

Thankfully, the silver lining of exorbitant legal fees—aside from winning your case—is being able to put this spend toward a new credit card’s welcome offer. Depending on how high your bill is, you may even be able to split it into two separate payments, enabling you to earn two welcome offers on two separate cards.

The majority of medium-sized and large law firms accept credit card payments, and even small firms have begun accepting credit cards.

Funeral Expenses: Make the Trip Your Loved One Always Wanted

If your loved one had a life insurance policy or already prepaid their funeral, managing it may be somewhat easier. However, money may still be tied up in probate, in which case you’ll need to cover the funeral costs upfront.

The average cost of a funeral in the U.S. is between $6,280 and $8,300, according to the National Funeral Directors Association.

Fortunately, the widespread majority of funeral directors accept credit card payments. This would allow you to earn a new credit card’s welcome offer in a single transaction, enabling you to make a trip in memory of your loved one at a low cost.

Using Virtual Cards for Emergencies: Unlock Instant Spending

Large unforeseen expenses are music to the ears of points and miles enthusiasts. However, to put that medical bill or attorney’s invoice toward a welcome offer, you’ll first need to apply for a new credit card (assuming you’re not already working toward a welcome offer).

It’s important to consider your time-frame. If the bill is due in a few days and you’d have no other way to earn the card’s welcome offer, applying for a new credit card could be a risky move.

While many card issuers offer the possibility of instant virtual credit cards—allowing you to begin spending upon approval instead of having to wait for your physical card to arrive in the mail—it’s never a 100% guarantee.

American Express often approves cards instantly upon applying. Once you’re approved, you’ll get instant access to your new card’s details, as long as Amex can verify your identity.

Instant card details are available for all Amex cards except the Amazon Business Card and Amazon Business Prime Card. Similarly, co-branded Amex cards will only be eligible for spending with their respective merchants until your physical card arrives, making them unsuitable for covering emergencies in a pinch.

Premium Amex cards, such as American Express Platinum Card® and the American Express® Gold Card, enjoy expedited shipping of one to three days, while all other cards can take seven to 10 days to arrive.

Likewise, Capital One also offers certain cardholders access to their new Capital One card number through the Capital One app upon approval. However, this feature is often available to existing Capital One cardholders only.

If you’re out of luck, it can take seven to 10 days for your Capital One card to arrive, unless you applied for the Capital One Venture X Rewards Credit Card, in which case shipping will be expedited.

Chase also offers instant approvals and allows you to begin spending with your card before your physical card arrives through Chase’s Spend Instantly feature. However, you can only use it via a digital wallet, so your merchant will need to accept digital wallet payments. Likewise, be aware that Mastercard, Amazon and Chase Business credit cards can’t be added to a digital wallet before the physical version of your card has arrived.

That said, you can expedite delivery without paying anything extra, to ensure you get your physical card within two days.

Some Citi cards offer an instant number/virtual account number; availability and limits vary by card. Keep in mind that Citi allows you to view your card number only once, so ensure to note it down or take a screenshot of it. Similarly, some data points suggest that you’ll only receive part of your credit limit until your physical card arrives, so take this into consideration when planning to use it for emergency spending.

Likewise, Citi small business cards and co-branded cards typically aren’t eligible for instant card numbers.

Best Credit Cards for Emergencies

The above examples are just some instances where you can be hit by unforeseen expenses. By turning these expenses into opportunities to earn points, you can take some of the sting out of them.

When it comes to paying for these expenses, you have two options:

- Putting the expenses toward a minimum spend-based perk, such as a welcome offer, free night award or companion pass

- Charging the expenses to a credit card with a high baseline rewards rate

The most lucrative choice is option No.1.

If you have a vet’s bill for $3,000, you could easily put that spend toward your new credit card’s welcome offer and reach the minimum spend in a single transaction.

If you’re looking at a higher bill approaching $8,000 or more, you could either shoot for a card with a higher minimum spend attached to its welcome offer or spread the payment across two separate cards, enabling you to earn two welcome offers.

Welcome offers aren’t the only minimum spend-based perk that you can put these unforeseen expenses toward earning. For example, if you’re working toward earning a Southwest Companion Pass, you could charge these expenses to a Southwest personal or business credit card, putting you closer to earning the 135,000 Rapid Rewards points required.

Likewise, there are a number of other co-branded airline credit cards with companion passes you can earn by reaching annual minimum spends, including:

- Aer Lingus Visa Signature Credit Card

- Atmos™ Rewards Ascent Visa Signature® Card

- British Airways Visa Signature Credit Card

- Iberia Visa Signature Credit Card

Aer Lingus Visa Signature® Card

75,000

Avios

after you spend $5,000 on purchases within the first three months of account opening

Annual Fee: $95

British Airways Visa Signature® Card

Earn 75,000

Avios

after you spend $5,000 on purchases within the first three months of account opening.

Annual Fee: $95

Alternatively, there is a wide range of co-branded hotel credit cards that offer a free night award when you charge a certain amount to your card within a calendar year, including but not limited to:

- Hilton Honors American Express Surpass® Card

- World of Hyatt Credit Card

- Marriott Bonvoy Bountiful® Credit Card

If you’re not looking to open any new credit cards or you need to pay the expense immediately, the second option is to charge the expense to an existing credit card. You’ll want to select a card that has a high baseline rewards rate on non-bonus category spending, given that most of these expenses fall outside of typical bonus spending categories.

Hilton Honors American Express Surpass® Card

Earn 130,000

Bonus Points plus a Free Night Reward

after you spend $3,000 in purchases on the Card in the first 6 months of Card Membership. Offer Ends 4/15/2026.

Annual Fee:

$150

The World of Hyatt Credit Card

Earn up to 60,000

Bonus Points

Earn 30,000 Bonus Points after you spend $3,000 on purchases in your first 3 months from account opening. Plus, up to 30,000 more Bonus Points by earning 2 Bonus Points total per $1 spent in the first 6 months from account opening on purchases that normally earn 1 Bonus Point, on up to $15,000 spent.

Annual Fee: $95

Here are some of the top cards with high baseline rewards rate to cover emergency spending:

- Chase Freedom Unlimited®: 1.5% cash back on non-bonus category spending

- Capital One Venture Rewards Credit Card: 2X Miles per dollar spent on non-bonus category spending

- The Blue Business® Plus Credit Card from American Express (see rates and fees): 2X points on all spending up to $50,000 per calendar year, then 1X points thereafter.

- Citi Double Cash® Card: 2% cash back on all eligible spending (1% when you buy and 1% when you pay for those purchases)

These are just a few examples of credit cards that earn a solid return on the unforeseen expenses of life.

Earn a $200

Bonus

after you spend $500 on purchases in your first 3 months from account opening.

Capital One Venture Rewards Credit Card

LIMITED-TIME OFFER: Enjoy $250

to use on Capital One Travel

in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

Annual Fee: $95

The Blue Business® Plus Credit Card from American Express

15,000

Membership Rewards®

after you spend $3,000 in eligible purchases on the Card within your first 3 months of Card Membership

Citi Double Cash® Card

$200

cash back

after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

Should I Apply for a New Credit Card to Cover the Expense?

Taking advantage of large unforeseen expenses by earning a new credit card’s welcome offer is the best way to make lemonade out of life’s lemons. However, you need to work out whether you’ll have enough time to apply for a new credit card and charge the expense to it.

While many card approvals happen instantly, some can take up to a week or longer. Assuming you’re approved, some card issuers will issue you a digital card that you can begin using immediately while you wait for your physical card to arrive in the mail.

However, you shouldn’t necessarily bank on this happening, particularly if you won’t be able to reach the card’s minimum spend without charging the unforeseen expense to it because certain card issuers don’t offer instant card numbers upon approval.

So if you’re tight on time and you’d be unable to earn your card’s welcome offer without charging the unforeseen expense to it, you’re best off using an existing credit card to cover the expense. However, if you have time to pay the bill and you could earn the welcome offer by other means (in the worst case), then it’s safe to apply for a new card.

Will I Get Extended Warranty and Purchase Protection Benefits?

An added benefit of paying for certain unforeseen expenses with a credit card is that you may be eligible for extended warranty and purchase protection benefits in certain cases.

Extended warranty benefits typically extend eligible U.S. manufacturer’s warranties by an additional year while purchase protection benefits can reimburse you within the first 60 to 120 days after purchasing a product in the event of loss, theft or accidental damage.

However, you’d need to purchase the product directly using your credit card, be it new parts for your car or hardware for your home. Similarly, there are exclusions to watch out for.

Therefore, you’re best off contacting your card issuer directly to see if a prospective purchase would be covered by their respective extended warranty and/or purchase protection policy. If they do cover it, any additional credit card processing fees tacked on by the merchant could be worthwhile paying for this added protection benefit.

Final Thoughts

Leveraging your everyday expenditure to earn you a return in the form of points and miles is the bread and butter of the credit card rewards game. So it’s no different when it comes to life’s unexpected expenses, be it an unwelcome vet bill, hospital bill or car repairs.

If you’ve just opened a new card or if you have the ability to apply for a new card, you could earn its welcome offer in a single payment, enabling you to fund an award flight, hotel stay or even both using the points earned. If you’re not working toward a welcome offer, you could still score yourself a minimum-spend based perk, such as a companion pass or free night award, or earn tens of thousands of points by charging the expense to a credit card with a high baseline rewards rate.

To learn how to maximize every dollar, dime and cent spent, check out the free 10xTravel course today.

New to the world of points and miles? The Chase Sapphire Preferred® Card is the best card to start with.

With a bonus of 75,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening. , 5x points on travel booked through the Chase TravelSM Portal and 3x points on restaurants, streaming services, and online groceries (excluding Target, Walmart, and wholesale clubs), this card truly cannot be beat for getting started!

Editors Note: Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

10xTravel is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. All values of Membership Rewards are assigned based on the assumption, experience and opinions of the 10xTravel team and represent an estimate and not an actual value of points. Estimated value is not a fixed value and may not be the typical value enjoyed by card members.

Editors Note: Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

bonus cash back

after you spend $6,000 on purchases in the first 3 months from account opening

to use on Capital One Travel

in your first cardholder year, plus earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening - that’s equal to $1,000 in travel

bonus points

after you spend $5,000 on purchases in the first 3 months from account opening.

Membership Rewards® Points

after you spend $6,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you’re approved and find out your exact welcome offer amount – all with no credit score impact. If you’re approved and choose to accept the Card, your score may be impacted.